{kind=link}

This article was submitted by Michael Stark, an analyst at Exness.

The dollar generally recovered in February and gold also bounced after late January’s dramatic retracement against the backdrop of somewhat greater uncertainty about the likely policies of the Federal Reserve (‘the Fed’) later this year and overall mixed data from the USA. Meanwhile the yen received a significant short-term boost from the clear results of the Japanese general election; the pound declined overall amid ongoing political intrigue and generally weaker economic performance. This article summarises these developments from last month, looks ahead at possibilities for the Fed’s upcoming meeting and briefly analyses the charts of XAUUSD, GBPUSD and USDJPY.

Mixed American data and the Fed’s possibly lower dovishness

2026’s first minutes from the FOMC showed policymakers divided on whether and how to proceed with loosening policy this year. December 2025 saw a significant shift in expectations for the first cut in 2026, being pushed back from April to June, while now there’s a nearly even probability of another hold and a single cut by June. The first clear majority expecting at least one cut to 3.25-3.5% is in July. Preliminary GDP for the fourth quarter of 2025 was significantly lower than expected:

1.4% was less than half the consensus of about 3% and less than a third of Q3 2025’s unexpectedly positive 4.4%. Consumer spending continued to grow last quarter but at a slower pace while government spending obviously contracted significantly due to the shutdown in October. Exports contracted slightly in Q4 after having grown very strongly the quarter before.

US Supreme Court’s challenge to the government’s sweeping tariffs is also likely to contribute to greater focus on this area in March compared to February when tariffs generally took a backseat in general news to the Epstein files and the American military buildup in the Gulf. The likelihood of a major war between the USA and Iran remains questionable for various reasons but traders of gold and oil in particular will continue to monitor any escalation as negotiations haven’t shown significant progress.

February’s NFP was significantly stronger than expected at 130,000, the highest by far since December 2024, and unemployment also unexpectedly declined slightly. This could challenge the prevailing narrative of a consistently slower American job market, but it’s too early to confirm this from just one job report. With strong jobs, at least in the immediate past, annual headline inflation still clearly above target at 2.4% and much weaker growth last quarter, the Fed’s reaction remains somewhat unclear.

Traders might find more clues about future policy from March’s inflation and especially the Fed’s press conference on 18 March. The funds rate is practically certain to be held at the current 3.5-3.75% then with a probability of about 95% according to CME FedWatch.

Challenges for the pound between dovishness and weaker jobs

The Bank of England (‘the BoE’) gave traders a surprise on 5 February by returning a majority of only one in favour of holding rates at 3.75%, with four members of the Monetary Policy Committee voting to cut. This solidified further expectations for a cut by the BoE in March; two or possibly three cuts in total are likely in the rest of 2026.

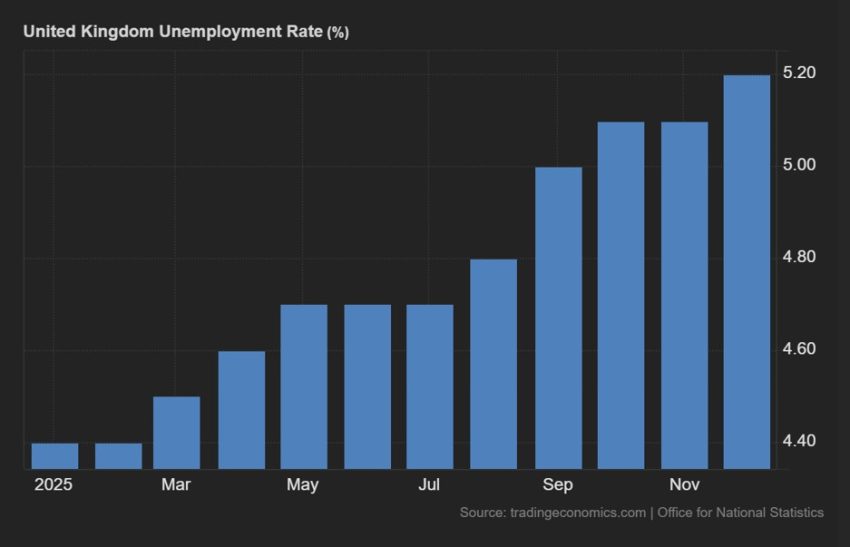

Early to mid February saw more political intrigue in Britain as the Prime Minister Keir Starmer faced scandal over his previous support for Peter Mandelson and there were rumours of his replacement as PM and leader of the Labour Party. This died down later last month, but the pound took a hit from 17 February’s significantly weaker job data from Britain:

British unemployment hit a five-year high at the end of 2025 as part of an ongoing but not very consistent trend of weakening in the labour market. This is certainly one factor driving more dovish expectations for the BoE’s policy as summer approaches.

19 March is particularly important for the pound’s upcoming direction because unusually both the job report for January-February and the BoE’s meeting will occur on the same day. Traders will analyse whether the trend of higher unemployment might continue and particularly how large the majority in favour of cutting might be on the MPC.

Electoral boost for the yen but policy likely to stay loose

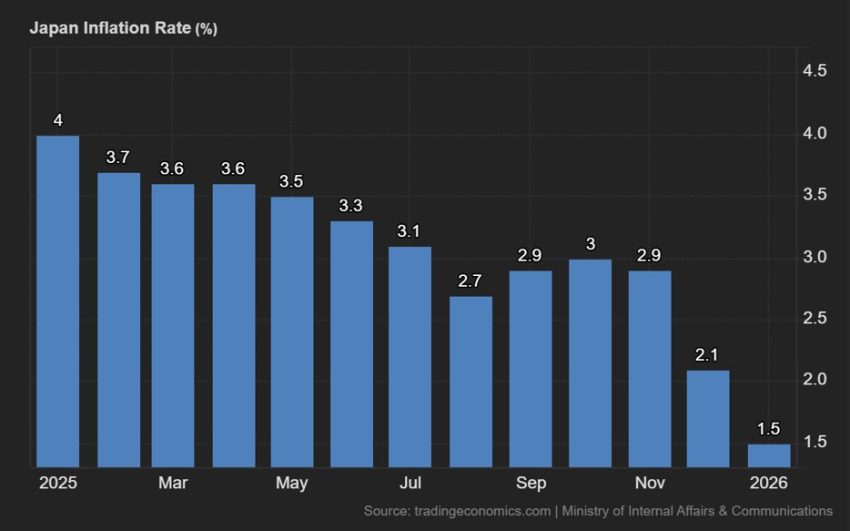

February’s Japanese general election was exceptional for delivering a landslide victory to the coalition government led by the Liberal Democratic Party of Prime Minister Sakae Takaichi. The LDP won more than 300 seats, by far its best result since its foundation in 1955 and indicating strong popular support for the government’s policies of fiscal support. The effects of these on inflation seem clear:

January’s annual headline inflation in Japan at 1.5% missed expectations by 0.4% and was the lowest in nearly four years. That inflation in Japan for this cycle definitely peaked in early 2025 means that further tightening by the Bank of Japan (‘the BoJ’) is highly questionable. The BoJ will announce its next decision on 19 March, the same day as the BoE, and traders will also monitor Japanese inflation on 23 March closely.

Gold holds $5,000 for now

Gold overall continued its recovery in February which started after the sudden decline at the end of January. Geopolitical risk remained at a similar level as the USA strengthened its military presence in the Gulf and senior politicians rattled their sabres here and there against Iran while the Supreme Court’s challenge to tariffs raised uncertainty about the government’s policies. However, recently stronger job data from the USA and some debate from the Fed’s latest minutes about the trajectory of rates were negative factors.

$5,000 remains the main technical reference for now with 20 February in particular showing a fairly strong gain to test $5,100. Volume remained lower around the middle of February with holidays in the USA and for Lunar New Year affecting demand. With the uptrend still active for now, a possible target for buyers might be somewhere in 28 January’s large up candle.

The 50 SMA from Bands around $4,800 might be a significant dynamic resistance which could cap any bout of losses barring a strong fundamental driver. The current incipient move above $5,100 might turn out to be a false breakout and presage a round of losses, but this depends on upcoming American data as well as sentiment and volume.

Cable pushes below $1.35 with more losses possible

Generally weaker British data for much of February contrasted with more positivity from the USA in early February to push cable down. However, the notably lower growth in America last quarter according to 20 February’s preliminary data combined with legal challenges to Donald Trump’s tariffs helped the pound recover some ground. March is very likely to bring a cut from the BoE while the Fed holds although both rates would still be in the same range.

The uptrend on the daily chart hasn’t clearly ended yet but volume has overall supported losses since late January. The price is quite close to the value area between the 100 and 200 SMAs, which is only slightly above the 23.6% weekly Fibonacci retracement, so the zone around $1.34 is a possible support from which a bounce might occur.

However, with the slow stochastic oversold and some buying volume starting to return around the end of February, it’d be possible to see a bounce back to the 50 SMA from Bands around $1.355. Traders are looking ahead to key American data early in March.

Double bottom around ¥152 for dollar-yen

Although the yen received a significant boost from the crystal clear results of February’s elections, notably weaker annual headline inflation in January was a negative factor which suggested that the BoJ’s recent limited hawkishness might not continue. With the Fed now not very likely to cut rates until July, the differential is likely to remain around 3% into the summer.

The now confirmed double bottom around ¥152 would normally suggest that the price is unlikely to break below there in the near future given that there’s no major data likely to drive a strong movement coming up immediately. The slow stochastic has recently completed an upward crossover in oversold and volume has generally remained high for much of February.

However, the upside is probably limited too given the focus in recent months on ¥160 as a likely area for intervention by the BoJ and possibly the Japanese government as well. Before that, the value area between the 50 and 100 SMAs might also cap gains. Dollar-yen in February was an exception among majors in that volume actually increased on average after the end of January rather than declining. Given the current fundamental environment, though, the price might move sideways overall in the near future barring a clear new signal from news.

The opinions in this article are personal to the writer; they do not represent those of Exness. This is not a recommendation to trade.