{kind=link}

The conflict in the Middle East may only be days old, but there are already major fears about the impact that soaring energy prices could have on people in the UK.

In particular, rising prices and energy bills could fuel higher inflation and see the Bank of England raise interest rates.

However, rising rates have knock-on effects elsewhere, including on people’s mortgages and savings.

Here, The Independent looks at how the war in the Middle East could impact your finances.

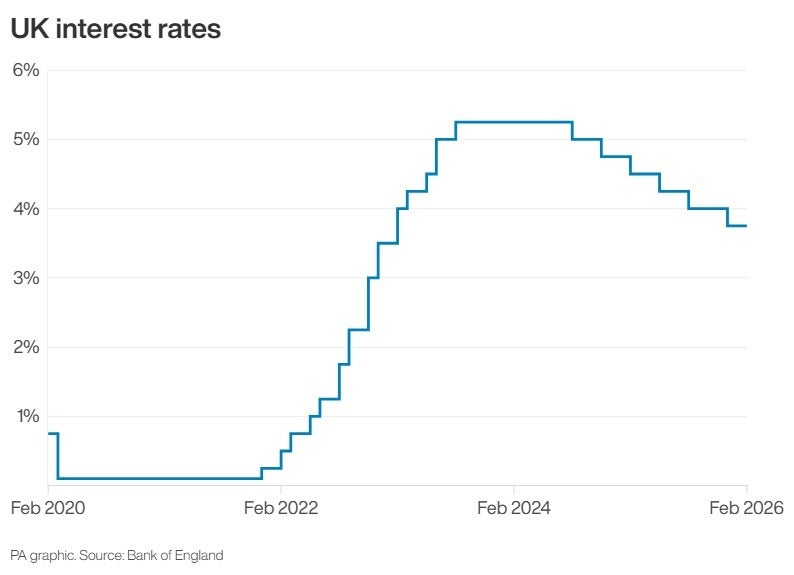

Interest rates

Interest rates were cut four times over the course of 2025, with the Bank of England (BoE) bringing down the main rate from a high of 5.25 per cent to the current level of 3.75 per cent.

That has been good news for mortgage holders, who have benefited from cheaper borrowing costs, and it was expected that interest rates could fall further – even with another rate cut possible when the BoE’s Monetary Policy Committee (MPC) meet on 19 March.

Some analysts were predicting three cuts across the course of 2026, bringing us back down to a base rate of 3 per cent which was last seen in December 2022. However, those analysts have quickly changed tune over the past week as geopolitical events once more threaten the global economy, with rising inflation once more a significant threat and interest rates likely to rise in response.

Mortgages

The potential consequences of the rising oil and gas prices include potentially higher food and goods costs, higher fuel prices and, if the situation is prolonged, an increase to mortgage deals through rising interest rates.

“Mortgage rates eased dramatically in 2025, helped by six interest rate cuts since August 2024, but the outlook today is very different from just a week ago,” said Alice Haine, finance analyst at Bestinvest.

“Shifting interest rate expectations are already filtering through to the market, with some major lenders announcing increases to their fixed-rate products in response to the crisis, and Moneyfacts data shows the average two- and five-year fixed deals have edged higher this week.”

Right now those are marginal adjustments; some have added 0.1 to 0.25 per cent onto a range of deals, similar to the amounts by which they were coming down each time across the past few weeks and months.

Get a free fractional share worth up to £100.

Capital at risk.

Terms and conditions apply.

ADVERTISEMENT

Get a free fractional share worth up to £100.

Capital at risk.

Terms and conditions apply.

ADVERTISEMENT

.jpeg)

Mortgage deals on the market typically alter in response to swap rates, which are contracts for payment between financial firms. When there is an expectation of future movements in the BoE’s base rate, swap rates may rise and fall ahead of time accordingly.

“Energy prices have risen sharply since the outbreak of the conflict because oil markets are highly sensitive to geopolitical tensions in the Gulf region. Any prolonged disruption to the supply of oil and gas poses a significant risk to the global economy and the outlook for inflation,” said Ms Haine.

“Persistent increases in energy prices would push inflation higher and slow economic growth, placing central banks around the world, including the BoE, in a very challenging position.

“The BoE has worked hard to contain the runaway price rises seen at the height of the cost-of-living crisis just a few years ago. Between December 2021 and August 2023, the Bank raised interest rates 14 times to curb excess demand and bring inflation under control.”

Britain’s housing market has not been in great shape over the past 12 months but there had been signs of improvement recently, with an increase in first time buyer activity being boosted by those falling mortgage rates.

Halifax’s house price index showed prices rose again in February of this year, up 0.3 per cent to an average property price of just over £301,000.

Another spike in mortgage costs might threaten to derail that progression, which is an important part of growing the UK economy.

One industry expert is remaining optimistic about the situation, however.

“The market was pricing in two cuts this year and it’s now pricing in one, but I still think we’ll get three,” said Tom Bill, head of UK residential research at Knight Frank, citing a weak labour market and wider inflation having been headed downwards.

“Even if we have a little bit of a blip. For markets to price back in two or more cuts, the first thing we need to see is energy prices coming back down. The second is more data of the kind we were getting earlier this year, including relatively anaemic economic growth.”

Savings

The other side of the household finances equation to mortgages is savings.

.jpeg)

When interest rates go up, people with money in the bank can typically benefit from it as they are able to earn a better return on their cash. For some time the best easy access rate on the market has been at 4.5 per cent with Chase, but already this week there have been one or two signs that others are upping their rates to compete with that, including in some cash ISA providers.

It is not yet certain that the BoE will raise interest rates further but a March “hold” call now looks increasingly likely, with another vote in April perhaps offering a better chance to assess matters more than a couple of weeks after the attacks in Iran began.

“The UK’s sluggish economy, coupled with rising unemployment rates, increased speculation that the Bank of England might go as far as delivering three cuts over the coming year, but a March cut now looks extremely unlikely and the satnav which had been guiding us forwards now seems to be on the fritz,” said AJ Bell’s Danni Hewson.

With the ISA deadline of 5 April also drawing near, it’s a timely reminder for savers to both maximise their money’s earning potential, and also make use of tax-free allowances this year while they still can.